If you’ve ever found yourself borrowing money, then you’ve experienced debt firsthand. Whether it’s settling a lunch tab with a friend or managing student loans, debt is an integral aspect of financial transactions. It encompasses various forms, from credit cards to mortgages, each playing a significant role in individuals’ financial landscapes.

So, what exactly is debt? Simply put, it refers to the money one owes to another entity or individual, which must be repaid over time, as outlined by the Consumer Financial Protection Bureau. Consumer debt, specifically, revolves around the goods and services consumed by individuals or households. This includes a wide array of financial obligations such as credit card debt, mortgages, home equity lines of credit (HELOCs), auto loans, student loans, medical debt, and personal loans. As of 2023, the total consumer debt balances in the United States amounted to a staggering $17.06 trillion, as reported by the Federal Reserve Bank of New York.

When delving deeper into the realm of debt, it’s essential to understand its various forms. According to Capital One, debt can manifest in several types, each operating distinctively:

- Secured Debt: This type of debt is backed by collateral, wherein an asset of equivalent value to the debt serves as security. In the event of default, the lender can seize the collateral to recoup the outstanding amount. A prime example of secured debt is a mortgage, where the borrower’s home acts as collateral. Failure to make mortgage payments could result in foreclosure, leading to the loss of the property.

- Unsecured Debt: Unlike secured debt, unsecured debt lacks collateral backing. This category encompasses financial obligations such as student loans and certain credit cards. Without collateral, lenders rely on other factors such as creditworthiness and income to assess borrowers’ repayment capabilities.

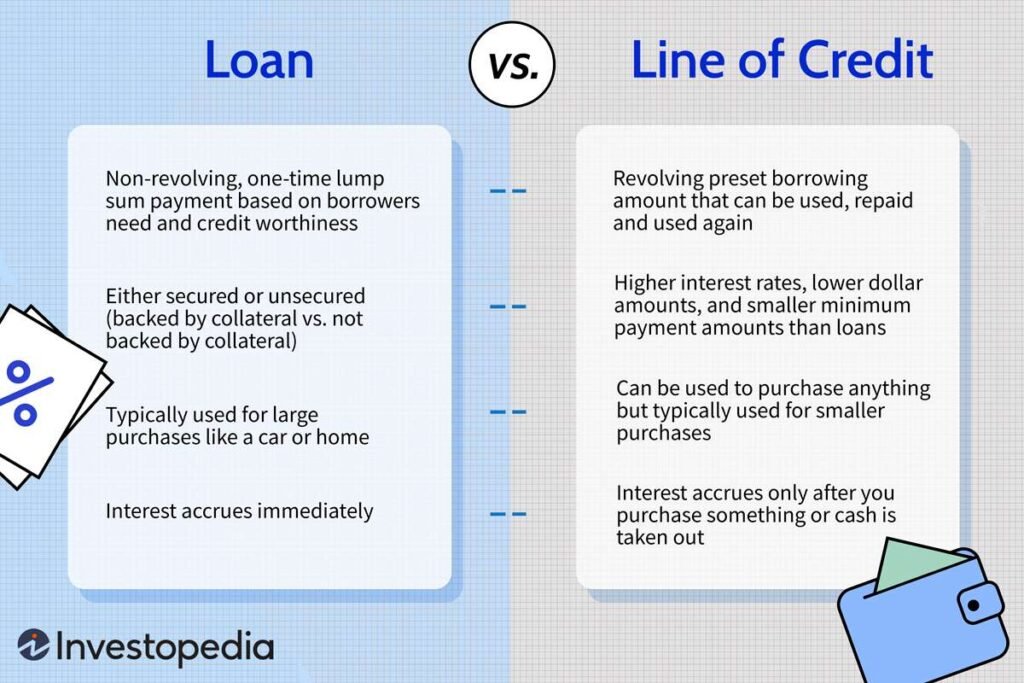

- Revolving Debt: Also known as open-ended credit, revolving debt allows borrowers to access funds as needed, with repayment flexibility contingent upon maintaining a good standing account. Credit cards are a prominent example of revolving debt, wherein users can borrow funds up to a predetermined credit limit and repay the balance over time.

- Installment Debt: Under installment debt, borrowers receive the entire loan amount upfront and repay it in fixed installments over a specified period. Auto loans and personal loans are common examples of installment debt, wherein borrowers commit to regular payments until the loan is fully repaid.

In navigating the intricacies of debt, understanding these distinctions can empower individuals to make informed financial decisions. By recognizing the nuances of each debt type, borrowers can strategize repayment plans and manage their financial obligations more effectively.

In essence, debt serves as a fundamental component of modern financial systems, facilitating access to essential goods and services while enabling economic growth and opportunity. However, responsible management and prudent decision-making are paramount to ensuring that debt remains a tool for financial advancement rather than a burden.